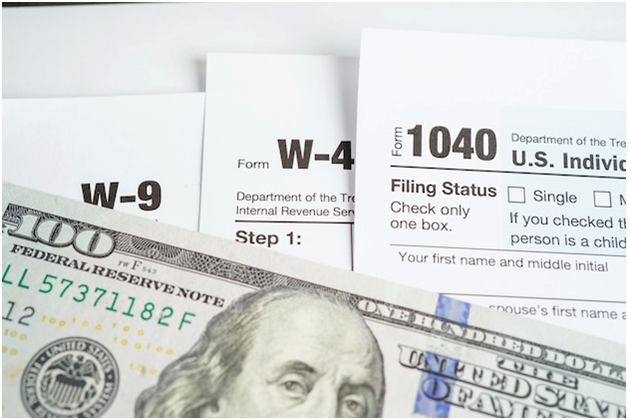

In past years, you could always rely on your tax refund to swoop in and save the day. But this year, the IRS warns Americans things could be different. Their forecasts reveal the average will drop down to roughly $2,000, more than a grand below last year’s peak. This news could spell trouble for many expectant Americans.

Nearly One-Third of Americans Are Dependent on Refunds

Roughly three-quarters of all Americans expect refunds from year to year. For many of them, it represents a nice boost to their usual budget in the spring. They might use this windfall to go on holiday, invest in a home sound system, or renovate their home.

But for roughly one-third of the country, refunds play a more important role in their everyday lives. A new study reveals nearly 30% of Americans rely on their tax refund to make ends meet. The share increases the younger you are, with 40% of Zoomers and 46% of millennials dependent on this windfall.

What Can You Do if You Receive Less?

When tax refunds can be as necessary as a paycheck, a cutback could be hard to handle. If the amount you’re due is less than you expected, don’t panic — there are some things you can do to smooth out your finances.

Delay Big Purchases or Repairs if Possible

You may have been waiting for your refund to arrive before you buy a new oven or make a household repair. Unfortunately, now might not be the time to make these changes if your windfall is smaller this year. You may have to delay these big expenses until you can save up what you need.

What happens if you were planning on using your refund to make a repair you can’t put off for another day? You can still handle this emergency expense, but you may have to borrow money.

Plenty of people use their credit cards to handle urgent, unexpected repairs. But if you’ve maxed out these accounts, an online personal loan may provide an alternative backup.

All you need is a phone to visit lender websites and review their rates and fees. Each lender may apply different charges, so it’s important you read this information clearly to understand the cost of borrowing in an emergency.

Talk to Your Creditors

Online personal loans are designed for non-recurring and unexpected emergencies. A bill, on the other hand, is a regular event; it usually arrives every month on a pre-determined date. Borrowing a personal loan everytime a bill arrives in your mailbox isn’t sustainable.

With online loans off the table, you should consider talking to your creditor. Let them know you want to pay your bill but are facing some difficulty.

Many businesses offer financing plans to help their customers pay them. Your arrangement could involve pushing out your due date until you have the money or paying back what you owe over installments. Just be aware these plans might cost money or apply interest, just like a personal loan.

Bottom Line:

A big tax refund might be a necessary addition to your finances, but it’s also a red flag; receiving a tax refund means you withheld too much tax on every paycheck throughout the year.

By tweaking your W-4 for next year, you can put more money in your pocket with each payday. This little bi-weekly boost could help you budget better for unexpected expenses and bills alike.

{kind=link}

{kind=link}